Project Report Preparation in India: What It Covers and How LegalBabu Prepares One That Gets Approved

Somewhere in India right now, an entrepreneur is sitting across a bank manager's desk. The idea is solid. The land is ready. The team is assembled. And the bank manager slides a form back across the desk and says - bring me a project report.

That is the moment everything stalls.

Not because the idea is weak - most of the time, it isn’t. Not because the business cannot succeed. But because nobody told this entrepreneur that the project report they submitted - the one they downloaded from some website, tweaked a few numbers in, and printed - is not what the bank actually needs. It is not what AICTE needs. It is not what CBSE needs. It is not what DGMA needs. And it is absolutely not what NABARD needs.

Project report preparation in India is the single most misunderstood step in the entire journey of building a business or an institution. Everyone knows they need one. Almost nobody knows what type they need, in what format, with what financial model, or built for which authority. That gap between knowing and knowing correctly is where millions of rupees, months of effort, and genuine opportunities go to waste.

This is everything you need to know about project report preparation - the types, the components, the process, and why LegalBabu prepares project reports that actually get approved.

What Is a Project Report, Really?

A project report is a formal, structured document that presents the complete technical, financial, legal, and operational blueprint of a proposed project or business. Banks use it to evaluate whether your project can repay a loan. Regulatory bodies use it to decide whether your institution meets their standards. Government subsidy bodies use it to verify whether your business qualifies for their scheme.

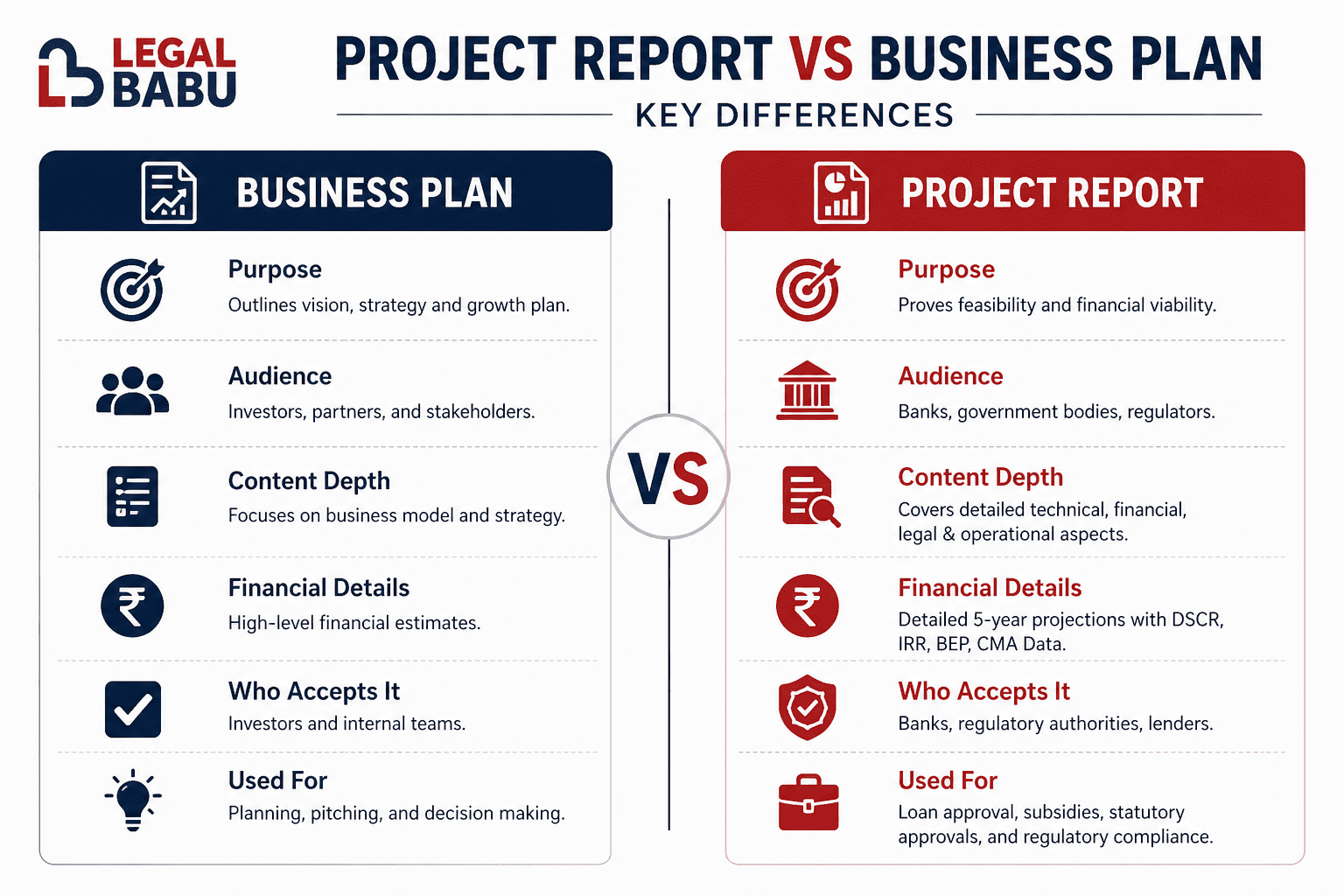

Here is the distinction that most people miss. A business plan is a strategy document. A project report is an evidence document. One explains your vision. The other proves it - with verified numbers, sourced market data, certified financial projections, and technical specifications that a trained evaluator can scrutinise line by line.

When you submit a project report to a bank or a regulatory body, you are not telling them your story. You are submitting your case. And just like a legal case, it has to be built correctly, in the right format, for the right audience, or it will be dismissed.

Project report preparation in India, therefore, is not about filling in a form. It is a discipline. Done right, it opens every door. Done wrong, it wastes everyone's time - yours most of all.

What are the Types of Project Reports Used in India?

Here is where things get genuinely interesting - and where most consultants let their clients down.

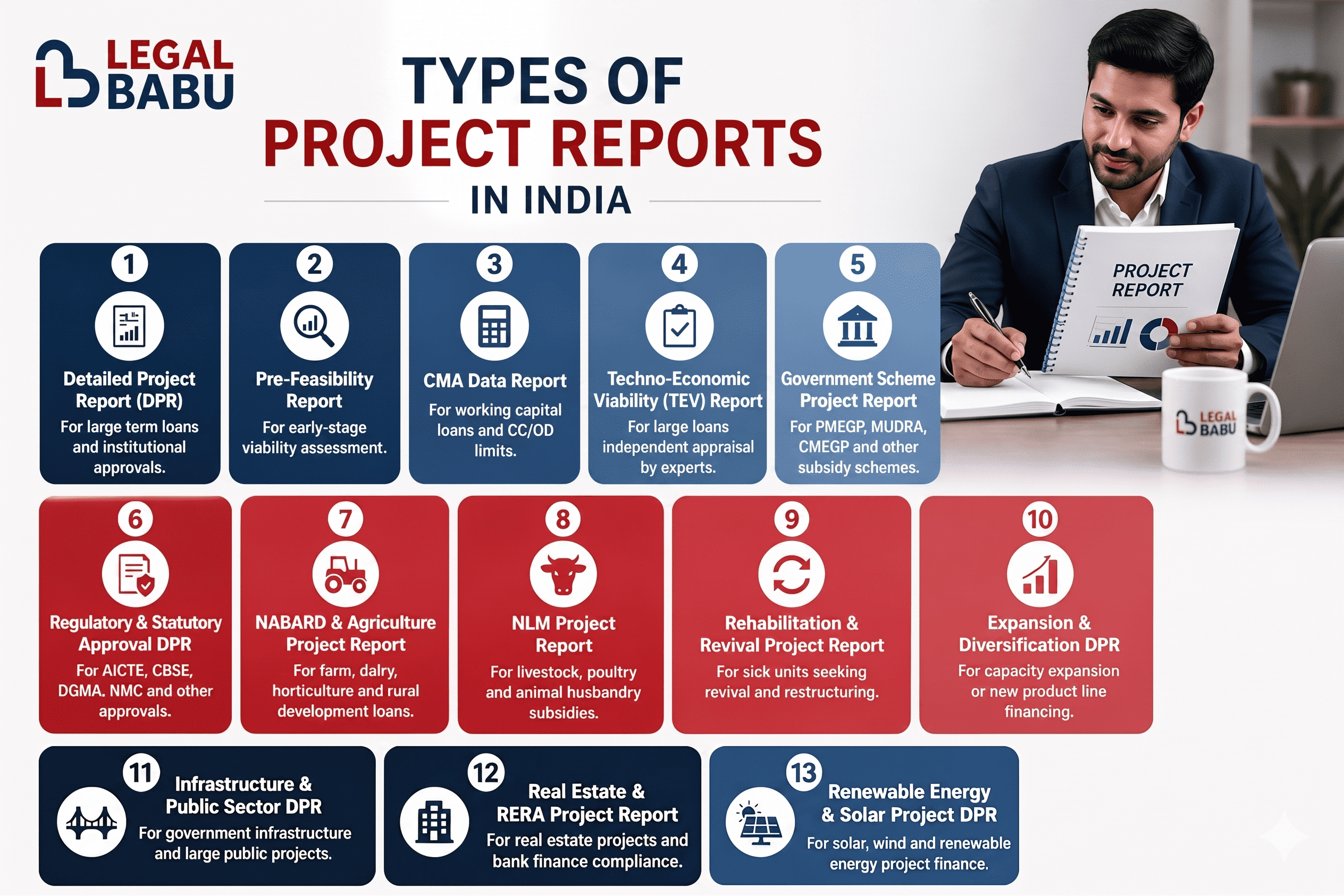

There is no single project report template that works everywhere. There are thirteen distinct types of project reports used across India, each built for a specific purpose, a specific authority, and a specific format. Submit the wrong type to the wrong authority, and your project report goes back to you, usually with a politely worded rejection and a request to resubmit.

Understanding which project report you need is step zero of the entire process.

1. Detailed Project Report (DPR)

The grandfather of all project reports. A DPR is the most comprehensive format - typically running 40 to 100 pages - and covers technical feasibility, financial modelling, market analysis, implementation schedule, and risk assessment. It is what banks want for long-term loans. It is what AICTE wants for engineering college approvals. It is what DGMA reviews for maritime institutions. When someone says "project report" without specifying a type, they usually mean a DPR.

2. Pre-Feasibility Report

Before you commit to a full DPR - before you hire a consultant, pay for a detailed market study, or finalise your project cost - you should know whether the project is worth pursuing at all. A pre-feasibility report answers that question. It covers broad cost estimates, regulatory requirements, market opportunity, and technology options. Think of it as the scouting report before the main campaign. Smart promoters commission this first. Most people skip it and then discover a fundamental problem six months in.

3. CMA Data Report

CMA stands for Credit Monitoring Arrangement. This is a structured financial statement format prescribed by the Reserve Bank of India for bank credit appraisals. It is mandatory for working capital loans, CC and OD limit applications, and most term loans above Rs. 25 lakh.

The CMA data report includes projected profit and loss, projected balance sheet, fund flow statement, and comparative performance across years - all in a standardised format that every scheduled bank in India accepts. It must be prepared by a Chartered Accountant. If your project report package is missing CMA data, the bank will send it back before the credit team even looks at it.

4. Techno-Economic Viability (TEV) Report

For large industrial loans - typically above Rs. 5 to 10 crore - banks commission an independent technical expert or CA firm to prepare a TEV report alongside your DPR. This is the bank's way of getting a second opinion. The TEV report independently verifies the technology you have selected, the reasonableness of your cost estimates, and the credibility of your revenue projections. A strong, detailed project report makes the TEV process faster and smoother. A weak DPR leads to a TEV report that essentially contradicts your numbers - and that is very hard to recover from.

5. Government Scheme Project Report

This is the project report format used for PMEGP, MUDRA Yojana (Kishore and Tarun categories), CMEGP, Stand-Up India, and Startup India applications. It is simpler in structure than a full DPR, but it has its own specific requirements - particularly around employment generation, social and economic impact, and scheme-specific compliance parameters.

The bank submits this project report to KVIC, KVIB, or the District Industries Centre for subsidy verification. Getting the format wrong here means the subsidy component is never released, even after the loan is sanctioned.

6. Regulatory and Statutory Approval DPR

This type of project report has nothing to do with financial viability in the bank sense. It is about institutional readiness, infrastructure compliance, and governance quality. AICTE requires it for engineering and management college approvals - and their 2024-27 Approval Process Handbook significantly revised the format, so any report built on the old structure will fail screening. CBSE requires it for school affiliation.

DGMA requires it for maritime training institute recognition and merchant ship registration. State health departments and the National Medical Commission require it for hospital approvals. Every authority has a different format. A hospital project report looks nothing like an AICTE project report. If you are setting up an institution, the entity structure must also be correct - whether that is a Trust, Society, or Section 8 Company - because the project report and the entity type must align.

7. NABARD and Agriculture Project Report

NABARD - the National Bank for Agriculture and Rural Development - has its own prescribed project report format, and it is completely different from a standard bank DPR. This type of project report is required for dairy farming, horticulture, fisheries, food processing, cold chain infrastructure, and rural development projects. It includes crop and livestock input costs, subsidy component calculations, farmer income projections, and NABARD's specific Term Finance eligibility criteria. Submit a standard DPR to NABARD, and the scrutiny officer will hand it back with a list of missing sections that you did not know existed.

8. NLM Project Report

The National Livestock Mission sits under the Ministry of Fisheries, Animal Husbandry and Dairying. Its project report type is distinct from NABARD reports and serves animal husbandry, poultry, goat farming, and piggery businesses seeking NLM subsidies. This project report covers breed selection, veterinary care protocols, feed conversion ratios, mortality rate assumptions, and the government subsidy calculation tied to that specific scheme.

It is submitted jointly to the State Livestock Mission office and the lending bank. Few consultants in India prepare these correctly. Most entrepreneurs never realise the difference until after rejection.

9. Rehabilitation and Revival Project Report

This is the least talked about type of project report, and also one of the most valuable to understand. It is prepared for existing sick or stressed business units - NPAs - that are seeking loan restructuring, One Time Settlement, or a turnaround under RBI's stress asset guidelines. Unlike every other project report type, this one is not proving a new idea. It is proving that a failed one deserves a second chance.

It must honestly diagnose what went wrong, present a credible and conservative turnaround plan, demonstrate revised repayment capacity, and show concrete promoter commitment. Banks are understandably sceptical when they read a Rehabilitation DPR. The project report needs to be thoroughly honest and thoroughly bulletproof at the same time. Very few consultants know how to balance those two things.

10. Expansion and Diversification Project Report

Your existing business is performing well. You want to add capacity, launch a new product line, or enter a new market. The bank wants a project report for the expansion loan. Here is what most entrepreneurs do not expect - the bank is going to look at your last three years of audited financials alongside your projections. Historical DSCR carries as much weight as projected DSCR. This type of detailed project report must therefore present past performance in a way that credibly supports future growth - not in a way that contradicts it.

11. Infrastructure and Public Sector DPR

Reserved for large government-funded projects - Smart City missions, AMRUT 2.0 infrastructure, metro rail corridors, port development under the Sagarmala Programme, and NHAI highway stretches. These project reports include PERT and CPM charts (mandatory for projects above Rs. 25 crore), ESG impact assessments, land acquisition timelines, and phased funding schedules. This is the domain of government contractors, Special Purpose Vehicles, and PSU-backed entities. The scale is different. The scrutiny is deeper. The format is more rigid.

12. Real Estate and RERA Project Report

Real estate developers in India need a two-layer document. The first layer is a RERA-compliant project disclosure under the Real Estate Regulation and Development Act, 2016 - covering land title, layout approvals, FSI utilisation, sales projections, and ESCROW fund management (RERA mandates 70% of collected funds be ring-fenced in a separate account). The second layer is a bankable DPR for construction finance. Both documents must be consistent with each other. If the numbers in your RERA disclosure contradict your bank DPR, you have a serious problem. Project report preparation for real estate requires both a legal lens and a financial one simultaneously.

13. Renewable Energy and Solar Project DPR

India is building solar capacity at scale. Every solar rooftop developer, Independent Power Producer, and wind energy project requires a detailed project report to access MNRE subsidies, DISCOM connectivity approval, and bank project finance. This project report is deeply technical. It includes site solar irradiation analysis, Capacity Utilisation Factor modelling, Power Purchase Agreement structure, grid connectivity design, operations and maintenance cost modelling, and IRR on energy yield over the asset life. For PM-KUSUM scheme applications for solar pumps, a simplified version of this project report is required. With MNRE targets pushing capacity addition at an accelerating pace, this type of project report is becoming one of the most frequently demanded.

Project Report Types at a Glance

|

Type |

Primary Use |

Submitted To |

|

Detailed Project Report (DPR) |

New project bank finance |

Banks, PSBs, NBFCs |

|

Pre-Feasibility Report |

Early-stage viability check |

Promoters / Investors |

|

CMA Data Report |

Working capital / CC-OD loans |

Banks - RBI mandated format |

|

TEV Report |

Large loan independent appraisal |

Bank-empanelled experts |

|

Govt Scheme Report |

PMEGP, MUDRA, CMEGP subsidy |

Banks, KVIC, DIC |

|

Regulatory Approval DPR |

Institutional recognition |

AICTE, CBSE, DGMA, NMC |

|

NABARD / Agriculture DPR |

Farm, dairy, and horticulture loans |

NABARD, Banks |

|

NLM Project Report |

Livestock and poultry subsidy |

State Livestock Mission, Banks |

|

Rehabilitation DPR |

Sick unit revival |

Banks, CDR Cell |

|

Expansion / Diversification DPR |

Capacity expansion loan |

Banks, NBFCs |

|

Infrastructure DPR |

Government infrastructure |

Ministry, NHAI, Smart City |

|

Real Estate / RERA DPR |

Housing project and bank finance |

RERA Authority, Banks |

|

Renewable Energy DPR |

Solar / wind project finance |

MNRE, DISCOM, Banks |

Project Report for Bank Loan - What Banks Actually Look For

Of every reason someone needs a project report in India, bank loan approval tops the list. Term loans, MUDRA Kishore and Tarun, PMEGP, working capital CC limits, project finance - every single one requires a project report before the bank even opens your file.

Banks are not reading your project report to understand your business. They are reading it to answer one question: Can this borrower repay the loan using the cash generated by this project?

Everything in the project report for bank loan approval exists to answer that from a different angle. The market analysis proves demand is real. The technical section proves the production plan is realistic. The financials prove the numbers work. And the DSCR settles it.

Banks in India require a minimum DSCR of 1.25 to 1.50. Below 1.0 means the project cannot service its own debt. That is a flat rejection - no discussion, no revision opportunity, no second chance on the same file.

|

What Banks Evaluate |

Why It Matters |

|

DSCR - minimum 1.25 to 1.50 |

Primary repayment indicator |

|

Promoter contribution - 25 to 30 percent |

Confirms skin in the game |

|

Total project cost breakdown |

Every rupee must be accounted for |

|

CMA Data in RBI format |

Mandatory for loans above Rs. 25 lakh |

|

Revenue projections with capacity ramp-up |

Year one at 100 percent is an instant red flag |

|

Working capital cycle |

Most amateur project reports skip this entirely |

|

Equipment quotations |

Cost claims without quotes are not accepted |

The most common rejection reason for bank loan project reports is not a bad idea - it is overconfident financial projections. Revenue at full capacity from month one. No seasonality. No ramp-up period. Banks have seen this a thousand times, and they do not believe it.

LegalBabu's CA team builds financial models calibrated to realistic capacity curves, with CMA data in the exact format your lender requires - whether that is SBI, an NBFC, or SIDBI for MSME finance. The Reserve Bank of India's project appraisal framework sets the standard. LegalBabu builds every bank-facing project report to meet it.

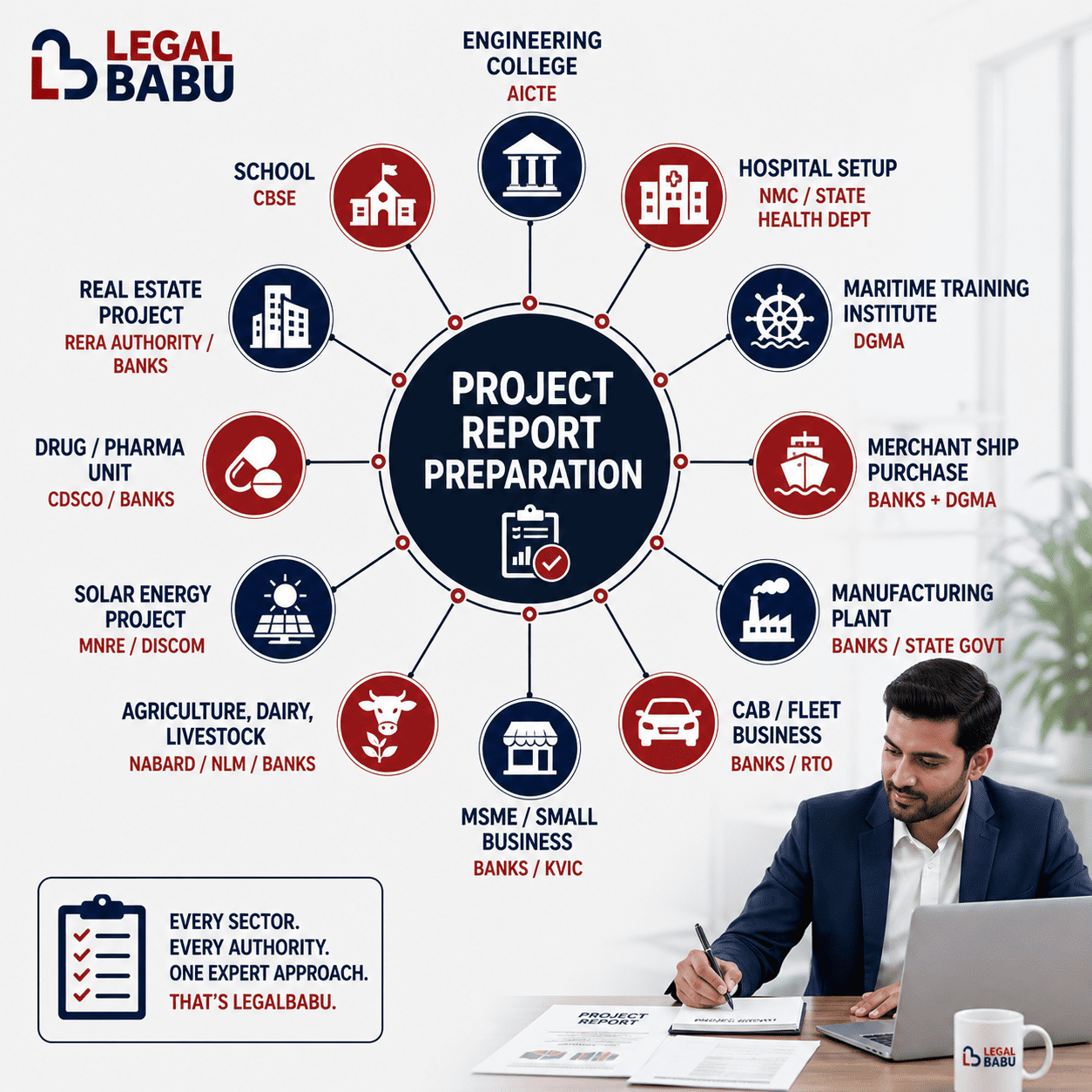

Who Needs a Project Report - Sector Wise

|

Sector |

Project Report Type |

Authority |

|

Engineering or Management College |

Regulatory DPR |

|

|

School |

Regulatory DPR |

|

|

Hospital or Nursing Home |

Regulatory DPR plus Bank DPR |

NMC, State Health Dept |

|

Maritime Training Institute |

Regulatory DPR |

|

|

Merchant Ship Purchase |

DPR plus TEV |

Banks plus DGMA |

|

Manufacturing Plant |

DPR plus TEV |

Banks, State Govt |

|

Cab or Fleet Business |

Govt Scheme Report |

Banks, RTO |

|

MSME or Small Business |

Govt Scheme Report plus CMA |

Banks, KVIC |

|

Agriculture, Dairy, Livestock |

NABARD DPR or NLM Report |

NABARD, Banks |

|

Solar or Renewable Energy |

Renewable Energy DPR |

MNRE, DISCOM |

|

Drug or Pharma Unit |

DPR plus Regulatory |

CDSCO, Banks |

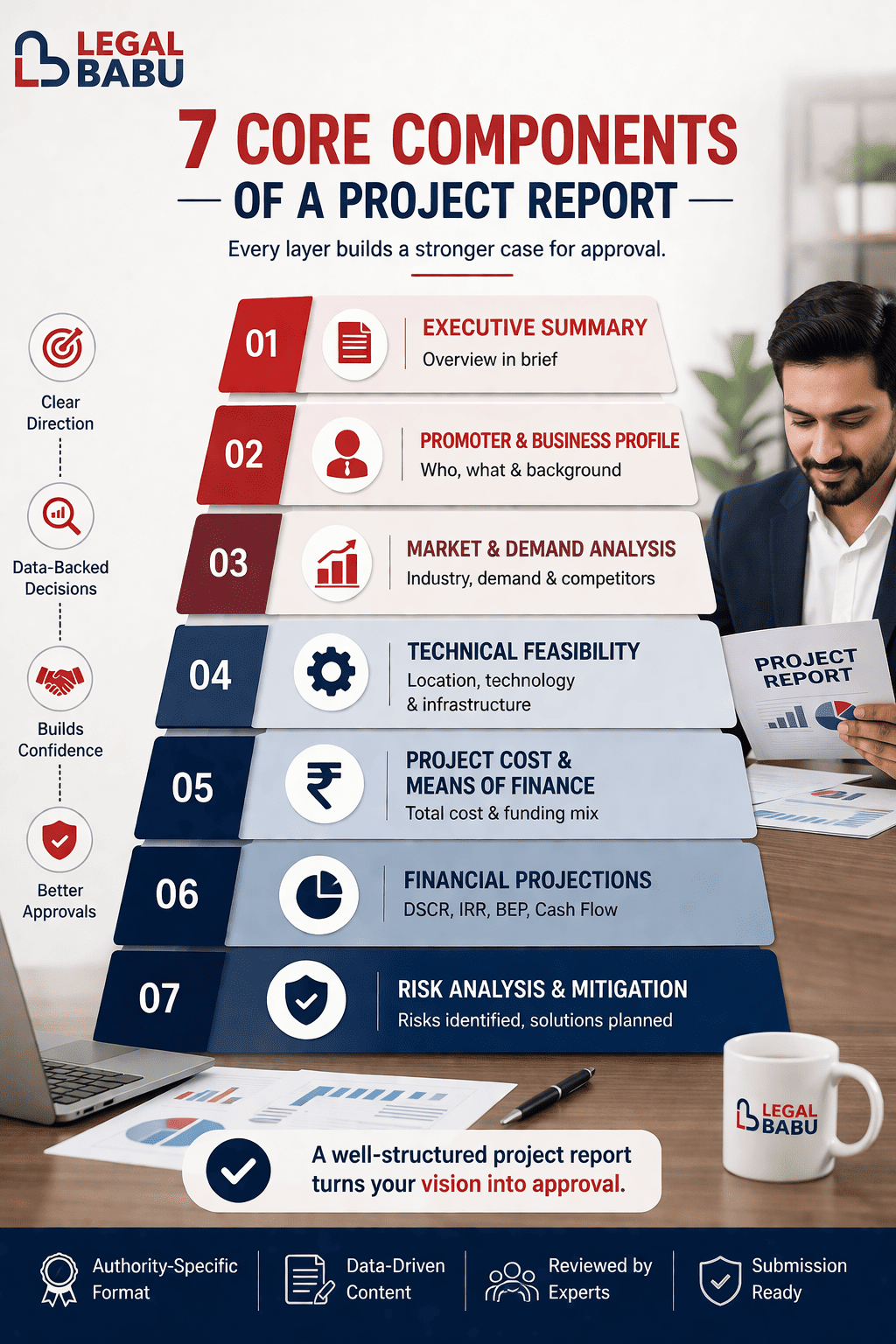

The 7 Components That Every Project Report Must Have

The format changes across types. The core does not. Every project report that clears scrutiny - whether from a bank credit team, an AICTE expert committee, or a NABARD appraisal officer - contains these seven elements. Skip one, and the report is sent back.

Executive Summary

The first page the reviewer reads. It covers what the project is, who the promoters are, how much is needed, and what the expected return looks like. You have about two minutes to make an impression here. Make them count.

Promoter and Business Profile

Legal entity details matter more than most promoters realise. Whether you are a Private Limited Company, Trust, Society, or LLP directly affects how the project report is structured and what supporting documents are required.

Market and Demand Analysis

Every claim in this section needs a source. The market is growing is not a data point. A cited industry report showing demand growth at a specific percentage, in a specific geography, for a specific product category - that is a data point. Banks and regulatory bodies have seen a thousand project reports built on vague assertions. Yours needs real evidence.

Technical Feasibility

Location, infrastructure, equipment specifications, technology choice, installed capacity, and manpower plan. For educational institutions, this section must align precisely with the norms set by AICTE - faculty-to-student ratios, laboratory equipment lists, and library standards.

Project Cost and Means of Finance

A complete cost estimate broken into land, building, machinery, pre-operative expenses, and working capital - with a clear funding split between promoter equity, bank loan, and any subsidy component. Every number must trace back to a quotation, a valuation, or an audited figure.

Financial Projections for Five Years

Projected profit and loss, projected balance sheet, cash flow statement, break-even analysis, IRR, and the figure every bank credit officer goes to first - DSCR. Banks require a minimum Debt Service Coverage Ratio of 1.25 to 1.50. A DSCR below 1.0 is an automatic rejection, no matter how well everything else is written. LegalBabu's CA team builds financial models specifically calibrated to pass bank stress-testing.

Risk Analysis and Mitigation

The section most people skip because it feels like you are listing reasons your project might fail. It is actually the opposite. A well-written risk section shows the reviewer that you have thought the project through completely and have a plan for every scenario. Authorities reject project reports that skip this. They approve the ones that address it confidently.

Why Most Project Reports Get Rejected

The rejection rate for project report submissions in India - across banks and regulatory bodies both - is high enough to be alarming. The reasons are almost always the same.

Copy-pasted financial projections that look identical across different industries and different project scales are spotted immediately by any experienced credit analyst. A generic template submitted to AICTE in the old format, after the 2024-27 handbook revised the structure, fails at the screening stage before it reaches any technical committee. Missing documents - no land proof, no state NOC, no entity registration certificate - result in rejection regardless of how good the financial model is. Market analysis with no citations, no data sources, and no competitive benchmarking gives a reviewer no basis to trust the demand projections. DSCR figures that are suspiciously high raise red flags rather than confidence.

Each of these failure points is preventable. Not after rejection - before submission. That is the entire point of working with a team that knows what these authorities are actually looking for.

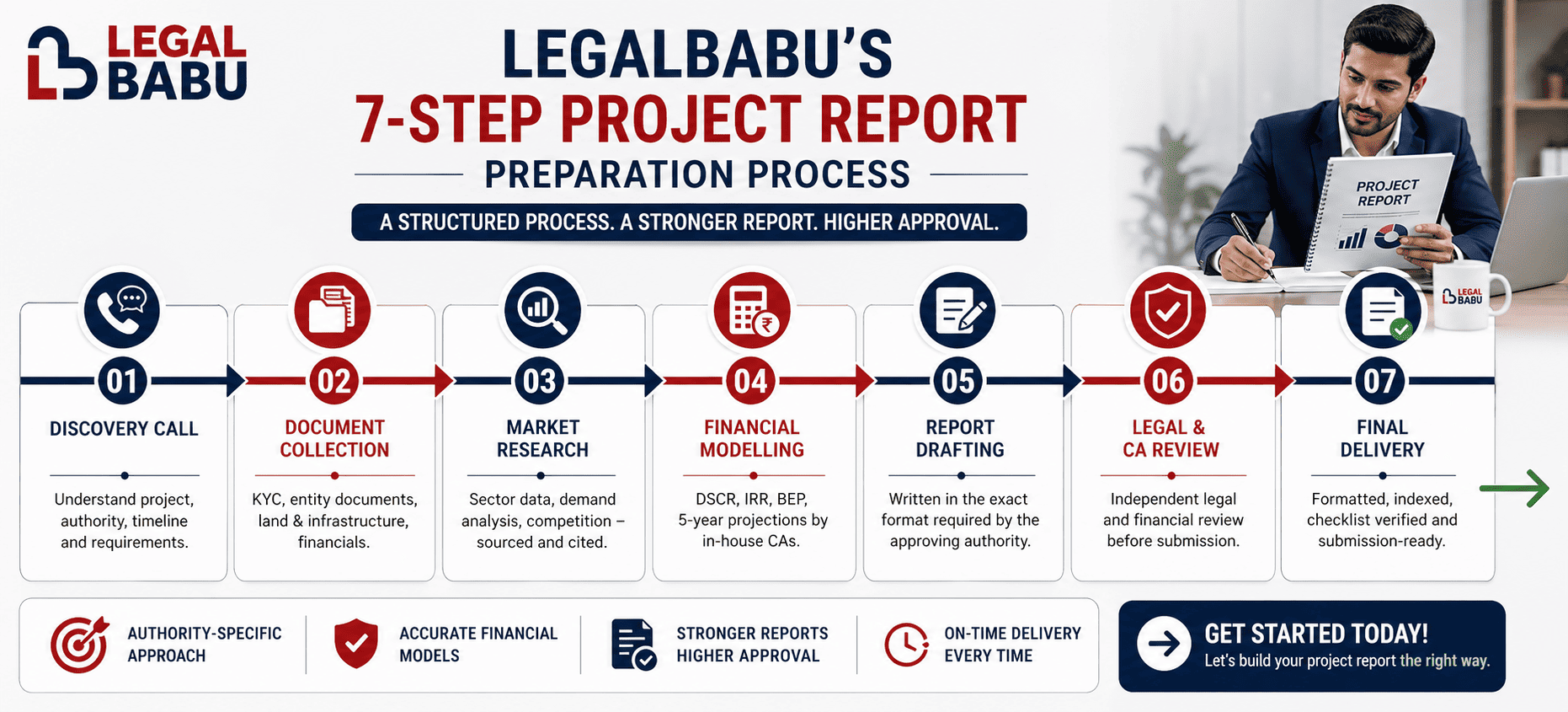

How LegalBabu Prepares a Project Report That Clears

At LegalBabu, project report preparation is a structured, authority-specific process. The starting point is always the authority receiving the report, because that determines everything about how the project report is built.

|

Step |

What LegalBabu Does |

|

Discovery Call |

Understand the project type, target authority, loan amount, and timeline |

|

Document Collection |

KYC, entity documents, land and infrastructure details, existing financials |

|

Market Research |

Sector data, demand analysis, competitive landscape - fully sourced and cited |

|

Financial Modelling |

Five-year projections, DSCR, IRR, BEP - built by in-house CAs to bank standards |

|

Report Drafting |

Written in the exact format required by the specific approving authority |

|

Legal and CA Review |

Independent review before client approval - catches problems before submission |

|

Final Delivery |

Formatted, indexed, document-checklist verified and submission-ready |

LegalBabu covers 20 plus sectors - education, maritime, healthcare, manufacturing, transport, MSME, agriculture, real estate, and renewable energy. The in-house team includes Chartered Accountants, legal advisors, and sector specialists who handle the work directly, not through outsourced vendors or recycled templates.

For maritime clients - those navigating MTO Registration or an RPSL License - LegalBabu prepares DGMA-specific project reports alongside the licensing process. For export-linked businesses, the project report is built alongside APEDA Registration and IEM Registration requirements. For regulated industries involving Drug License or CDSCO License applications, the project report is aligned with the compliance journey - not treated as a separate document that was prepared without context.

Document Checklist Before You Begin Project Report Preparation

|

Category |

What You Need |

|

Promoter KYC |

PAN, Aadhaar, address proof, photograph |

|

Business Entity |

Incorporation certificate, MoA/AoA, Trust Deed, or Society registration |

|

Land and Infrastructure |

Sale deed or lease agreement, building plan, local authority NOC |

|

Financial History |

Three years ITR for individual and entity, twelve months bank statements |

|

Project-Specific |

Equipment quotations, technology details, capacity plan, and site layout |

|

Regulatory Pre-Requirements |

State NOC for CBSE/AICTE, DGMA pre-approval letter, and health department NOC |

Every Door in India Opens with the Right Project Report

The engineering college that shapes careers. The solar farm that powers a district. The dairy operation that sustains a hundred farming families. The hospital that serves people who have never had access to quality healthcare. Every single one of them - at some point in their journey - needed a project report that someone reviewed, questioned, scrutinised, and finally approved.

Project report preparation in India is not a box you check on your way to the real work. It is the real work. It is the document that either earns your approval or stalls your entire plan for months or years.

LegalBabu prepares project reports that are approved for every sector, every authority, in the format they actually require. Not templates. Not copy-paste. Project reports are built to be clear.

Speak with a LegalBabu expert today and let us begin preparing your project report.

FAQS

FAQs about Project Report Preparation in India

-

What is the difference between a project report and a business plan?

A business plan is a strategic document built for planning and investor pitches. A project report is a formal financial and legal document submitted to banks or government authorities. It contains verified cost estimates, CMA data, DSCR calculations, and five-year financial models - all of which a business plan does not include. Banks do not accept a business plan in place of a project report.

- How many types of project reports exist in India?

- What is DSCR, and why do banks focus on it so heavily?

- How long does project report preparation take?

- Can the same project report work for a bank loan and an AICTE approval?

- Is a project report required for PMEGP?

- What makes a Rehabilitation DPR different?

- Does LegalBabu handle NABARD project report preparation for agriculture?

- Do I need a project report to purchase a merchant ship?

- What is a TEV Report?

- Can LegalBabu prepare a project report for a solar energy project under MNRE?

- What happens if my project report is rejected?