How to Get a Collateral-Free Loan Under CGTMSE?

So you have a business idea or maybe a running business, and you need funds to grow. You go to the bank, they listen to everything you say, and then they ask one thing: do you have any collateral? And right there, for a lot of small business owners in India, the entire conversation just stops. Because not everyone has a property to mortgage or land to pledge, especially if you are just starting out or you are a first generation entrepreneur who has built everything from scratch.

But here is what most people do not know. The government has a scheme that fixes exactly this problem. It is called CGTMSE, and if you qualify for it, you can get a business loan of up to Rs 10 crore without pledging a single asset. No property. No gold. No guarantor. Nothing.

Let us walk through the whole thing from scratch so you know exactly what this scheme is, whether you qualify, what it will cost you, and how you actually go about getting it.

What is CGTMSE?

As we all know, when you go to a bank for a business loan, the first thing they ask for is collateral. They want some kind of security, your property, your land, your gold, something. Because if you stop repaying the loan, the bank needs a way to recover its money. And if you do not have any asset to pledge, the bank simply refuses to give you the loan. This is the biggest problem that most small business owners in India face.

So the government came up with a solution for this, and that solution is called CGTMSE. The full form is Credit Guarantee Fund Trust for Micro and Small Enterprises. It was set up jointly by the Ministry of MSME, Government of India and SIDBI, which is the Small Industries Development Bank of India. You can check the official CGTMSE website for more details on the scheme.

Now let us understand how this actually works. Suppose you go to a bank and ask for a Rs 20 lakh business loan but you have no property to mortgage. Normally the bank would say no. But if the bank is registered under CGTMSE, what happens is that CGTMSE gives the bank a guarantee. It tells the bank, if this borrower defaults, we will cover your loss up to a certain percentage. Because of this guarantee, the bank no longer needs you to pledge any asset. You get the loan, and CGTMSE covers the bank's risk.

Now one thing you must be clear about is that this guarantee is not for you. It is for the bank. CGTMSE is protecting the bank, not you. But because the bank now has that protection, you end up getting a collateral-free loan. That is the whole idea behind this scheme. And if you want to understand how the government actually designs and funds schemes like this, reading about how the government earns and spends is a really good read.

Basic Features of a CGTMSE Loan at a Glance

Before we move ahead, let us quickly go through the basic features of this loan. Because before you start the application process, you should know exactly what this loan looks like in terms of amount, cost and tenure.

|

Feature |

Details |

|

Loan Amount |

Up to Rs 10 crore |

|

Collateral Required |

None |

|

Third Party Guarantee |

Not required |

|

Eligible Borrowers |

Micro and Small Enterprises (new or existing) |

|

Type of Loans Covered |

Term loans and working capital facilities |

|

Interest Rate |

Linked to the bank's MCLR or base rate; varies by lender and loan amount. CGTMSE does not fix a rate |

|

Repayment Tenure |

Decided by the lender; term loans typically up to 7 to 10 years |

|

Annual Guarantee Fee |

Starts from 0.37% for loans up to Rs 10 lakh; increases based on loan size (revised from April 2025) |

|

Processing Fees |

Charged by the lender as per their own policy; no fixed amount set by CGTMSE |

|

Who Pays the Guarantee Fee |

The lender pays CGTMSE; lender may or may not pass it on to the borrower |

|

Scheme Managed By |

CGTMSE (set up jointly by Ministry of MSME and SIDBI) |

Now one thing that a lot of people get confused about here is the interest rate and the repayment tenure. Many people assume that because this is a government backed scheme, there must be a fixed interest rate. But that is not how CGTMSE works. CGTMSE only decides the guarantee coverage and the guarantee fee. The interest rate, the tenure and the processing charges are all decided by the bank you are approaching. So when you sit down with your lender, make sure you discuss and negotiate these things directly with them.

How Does the CGTMSE Guarantee Coverage Actually Work?

As we discussed, CGTMSE gives a guarantee to the bank. But this guarantee is not for 100 percent of your loan. CGTMSE covers between 75 percent and 90 percent of the outstanding loan amount, and the exact percentage depends on who you are as a borrower and how much you are borrowing.

Let us understand this with the coverage breakdown:

|

Borrower Category |

Loan Amount |

Guarantee Coverage |

|

Women Entrepreneurs |

Up to Rs 5 lakh |

90% |

|

Micro Enterprises |

Up to Rs 5 lakh |

85% |

|

SC / ST Entrepreneurs |

Any amount |

85% |

|

North East Region, J&K and Ladakh |

Up to Rs 5 lakh |

80% |

|

All Other Borrowers (General) |

Up to Rs 10 crore |

75% |

|

Micro Enterprises (above Rs 5 lakh) |

Rs 5 lakh to Rs 10 crore |

75% |

Suppose you are a woman entrepreneur and you are taking a loan of Rs 4 lakh. In this case CGTMSE gives the bank a 90 percent guarantee. So if you default, the bank can recover 90 percent of the outstanding amount from CGTMSE. Because the bank's risk is almost fully covered, your chances of getting the loan approved without any collateral become much higher.

Now suppose you are a general category borrower and you are taking a loan of Rs 50 lakh. Here the coverage is 75 percent. The bank still has a guarantee on three quarters of the loan, which is a strong protection. But the remaining 25 percent is the bank's own risk. This is why some banks may still assess your repayment capacity carefully even under this scheme.

So the simple way to think about this is, the higher your coverage percentage, the more comfortable the bank feels, and the easier your loan approval becomes. And if you fall under a special category like women entrepreneur or SC/ST, this scheme benefits you even more than it does for a general borrower.

Who Can Apply for a CGTMSE Loan? Eligibility Explained

Now let us talk about who can actually apply because this is usually the very first question in everyone's mind.

Types of Businesses That Are Eligible

You are eligible if you are a new or an existing Micro or Small Enterprise. It does not matter if you are in manufacturing, services or trading, all three are covered. Your business can be structured as a proprietorship, a partnership firm, a Private Limited Company or an LLP. Any of these work fine.

What Registrations Do You Need?

Your business should fall under the MSME definition as per the MSMED Act and you need to have a Udyam Registration done. If you do not have that yet, that is literally the first thing you need to sort out before anything else, because without it your business does not even have an official MSME identity. If your loan amount is more than Rs 5 lakh, you will also need your IT PAN.

If you are also looking to understand how ease of doing business in India works and what registrations make your business more credible in front of a lender, that is a genuinely good read to go through before you walk into a bank.

What the Bank Looks For

Your business needs to look viable to the bank. They need to believe you can actually repay the loan. So your business plan and financials need to be solid. And one very important thing to know here is that you cannot go to just any bank. You have to approach a bank or NBFC that is a registered Member Lending Institution under CGTMSE. The official CGTMSE website has the full list of these institutions.

Who is NOT Eligible?

Agriculture businesses, Self Help Groups, Joint Liability Groups and educational institutions are not covered under this scheme. So keep that in mind before you apply.

Agriculture businesses, Self Help Groups, Joint Liability Groups and educational institutions are not covered under this scheme, so keep that in mind before you apply.

What Does CGTMSE Circular 259 Say About Credit Card Guarantee Coverage?

Now there is a very specific circular that CGTMSE has put out called Circular 259, and it talks about credit card coverage under the scheme. If you are a micro enterprise and you are looking at credit card based financing, this circular is directly relevant to you. You can check all the latest circulars including Circular 259 directly on the CGTMSE Circulars page. Let us just walk through what it says.

The maximum limit of the credit card under this circular is Rs 5 lakh per borrower. So if you are a micro enterprise and you have a credit card issued through a registered lending institution, you can get guarantee coverage on that card up to Rs 5 lakh.

The extent of guarantee coverage here is 75 percent of the amount in default or the credit card limit, whichever is lower, and this applies irrespective of the category of the borrower. So unlike some other CGTMSE coverages where the percentage changes based on whether you are a woman entrepreneur or an SC/ST entrepreneur, here it is a flat 75 percent for everyone.

Only credit cards that have a reference number from the Jan Samarth Portal, also called JSP, are eligible for this coverage. So if your card was not issued through the Jan Samarth Portal, it will not qualify under this circular.

Here is a quick summary so you can see all of this at a glance:

|

Parameter |

Details as per Circular 259 |

|

Maximum Credit Card Limit |

Rs 5 lakh per borrower |

|

Extent of Guarantee Coverage |

75% of amount in default or credit card limit, whichever is lower |

|

Eligible Cards |

Cards with reference number from Jan Samarth Portal (JSP) |

|

Primary Security |

Not mandatory |

|

Annual Guarantee Fee Rate |

0.55% on the credit card limit |

|

Risk Premium |

Not applicable (all beneficiaries are Micro Enterprises) |

|

Lock-in Period |

9 months from guarantee start date |

|

Validity of Guarantee Coverage |

5 years from date of issuance of circular |

|

Tenure of the Scheme |

3 years from launch or till 10 lakh cards are issued, whichever is earlier |

|

Credit Appraisal Responsibility |

Lending Institutions and Credit Card Issuers |

What Documents Do You Need to Apply?

Now let us talk about what you need to keep ready before you go to the bank. This part is really important because a lot of applications get rejected or delayed simply because the documents are not in order.

Basic KYC and Registration Documents

You need your Udyam Registration Certificate because without this your application simply does not move forward. You need your KYC documents which includes your Aadhaar card, PAN card and address proof like a utility bill or rental agreement. You also need proof of your business registration, so depending on your business structure it could be your Certificate of Incorporation, your Partnership Deed or your LLP Agreement.

Business Plan and Financial Documents

You need a detailed business plan or project report and this is where a lot of people make a mistake. They go to the bank with something very basic and wonder why the loan got rejected. Your business plan needs to clearly explain what your business does, how you plan to use the loan amount and how you will repay it.

You also need your financial statements like balance sheets, profit and loss accounts and bank statements for the last two to three years if your business is already running. If your loan is above Rs 5 lakh, your IT PAN is mandatory. It also really helps to have your income tax filing process and documents properly sorted before you walk into a bank, because lenders will ask for your ITR filings as part of the verification process. And if your business is also dealing with any MCA compliance matters, it is worth checking out the MCA compliance relief scheme 2026 before you apply.

This is exactly the part where LegalBabu really helps you. We help you prepare all your documents in the right format and make sure your business plan is bank-ready. A lot of loan rejections happen not because the business is weak but because the paperwork was incomplete or the project report was not convincing enough. We make sure that does not happen with you.

How to Apply for a CGTMSE Loan? Step by Step Process

Now let us go through the actual process because this is where most people need the most clarity.

Step 1: Get All Your Registrations Done First

The first thing you need to do is get all your registrations in place. That means your business registration, your GST registration and your Udyam Registration. If any of these are missing, the bank will not even consider your application. LegalBabu handles all of this for you so you do not have to run around figuring it out on your own. If you are also a startup and want to understand the new startup recognition and deep tech rules that can give your business additional credibility in front of lenders, that is worth reading too.

Step 2: Find a CGTMSE Registered Lender

Once your registrations are sorted, you need to find a bank or NBFC that is listed as a Member Lending Institution under CGTMSE. You cannot walk into just any bank and apply. It has to be a registered one. Check the official CGTMSE website for the complete list before you approach anyone. You can also go through the CGTMSE Circulars to stay updated on any recent changes under the scheme.

Step 3: Prepare and Submit Your Loan Application

Then you prepare your full loan application along with your business plan and all supporting documents and submit it to the bank. The bank will review your application, assess your repayment capacity and do their own due diligence. If you want to understand the full scheme guidelines as laid out by DCMSME, you can go through the official government scheme page as well to know exactly what the bank will be evaluating.

Step 4: Bank Applies to CGTMSE for the Guarantee

If the bank is satisfied with your application, they approve the loan internally and then they go to CGTMSE through their online portal to get the credit guarantee cover. You do not have to go to CGTMSE yourself. The bank handles that part entirely on your behalf.

Step 5: Pay the Annual Guarantee Fee

Once CGTMSE approves the guarantee, there is an Annual Guarantee Fee that needs to be paid. As per the latest structure effective from April 2025, this fee starts from 0.37 percent for loans up to Rs 10 lakh and goes up based on the loan amount. The lender decides whether to pass this fee on to you or absorb it themselves. Also, if the Budget 2026 tax changes affect your business finances in any way, that is worth understanding before you finalise your loan amount.

Step 6: Loan Gets Disbursed to Your Account

After the fee is paid and the guarantee is active, the bank disburses the loan directly to your business account. No collateral, no third party guarantee required. Just your business plan and your commitment to repay. The whole process from application to disbursement typically takes about two to four weeks depending on the bank and how well prepared your documents are.

What Happens if You Default on a CGTMSE Loan?

Now you might be wondering what happens if someone defaults. So if you default, the bank claims the guaranteed portion from CGTMSE and CGTMSE reimburses that amount to the bank. But this does not mean you are off the hook. You as the borrower are still legally liable to repay the loan. The guarantee is there to protect the bank, not to let the borrower escape repayment. So please do not think of this as a free loan. It is still a proper loan with proper repayment obligations and the bank can still take legal action against you for the remaining amount.

Benefits of the CGTMSE Scheme for Small Business Owners

Let us talk about why this scheme is genuinely a big deal for small business owners in India.

No Collateral Required at All

You do not need to put your house, your land or any other asset on the line. For first generation entrepreneurs who are building something from scratch, this alone is a massive relief.

Loan Amount Up to Rs 10 Crore

The scheme covers a very wide range of loan requirements, from a few lakhs all the way up to Rs 10 crore. So no matter what stage your business is at, there is a good chance this scheme can help you. And if you are also thinking about listing your business eventually, reading about SME IPO listing requirements in India will give you a sense of where this kind of funding can take your business in the long run.

Covers Both Term Loans and Working Capital

Whether you need funds to buy machinery or to manage your day to day business operations like buying raw material or managing inventory, CGTMSE covers both term loans and working capital facilities.

Special Benefits for Women, SC/ST and Borrowers from Backward Regions

Women entrepreneurs, SC and ST entrepreneurs and businesses in the North East Region, Jammu and Kashmir and Ladakh get higher guarantee coverage under the scheme. This makes it significantly easier for these categories to get their loans approved.

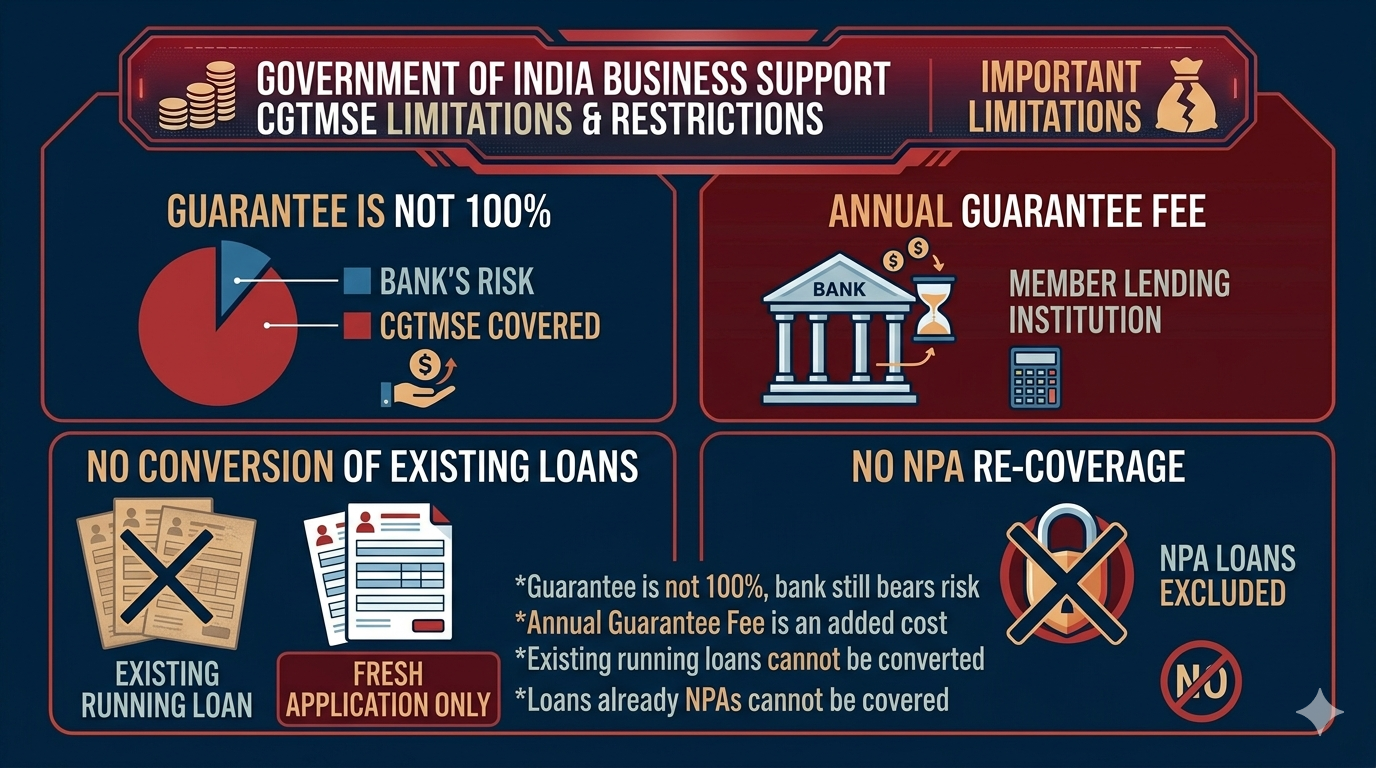

Limitations of CGTMSE You Should Know About

Despite how useful this scheme is, there are a few limitations you should know about before you apply so there are no surprises later.

The guarantee only covers 75 to 90 percent of the loan, not 100 percent, so the bank still bears some risk. The Annual Guarantee Fee adds a small cost to your overall borrowing. You cannot convert an existing running loan into a CGTMSE covered loan because the scheme only applies to fresh applications. And loans that have already turned into NPAs cannot be covered under this scheme either. If you want to understand how the government designs and funds schemes like this one, reading about how the government earns and spends gives you a really interesting perspective on the whole thing.

FAQS

FAQs on Collateral-Free Loan Under CGTMSE

-

What is CGTMSE and who set it up?

CGTMSE stands for Credit Guarantee Fund Trust for Micro and Small Enterprises. It was set up jointly by the Ministry of MSME, Government of India and SIDBI. The scheme gives a credit guarantee to banks and NBFCs so that they can give collateral-free loans to micro and small businesses without worrying about recovery in case of default.

- How much loan can I get under CGTMSE?

- Do I need to pledge any property or asset to get a CGTMSE loan?

- Who is eligible to apply for a CGTMSE loan?

- Can I apply for a CGTMSE loan directly without going through a bank?

- What is the Annual Guarantee Fee and do I have to pay it?

- Is Udyam Registration mandatory for this scheme?

- Does CGTMSE cover working capital loans or only term loans?

- Can women entrepreneurs get better coverage under CGTMSE?

- Can an existing loan be converted into a CGTMSE covered loan?